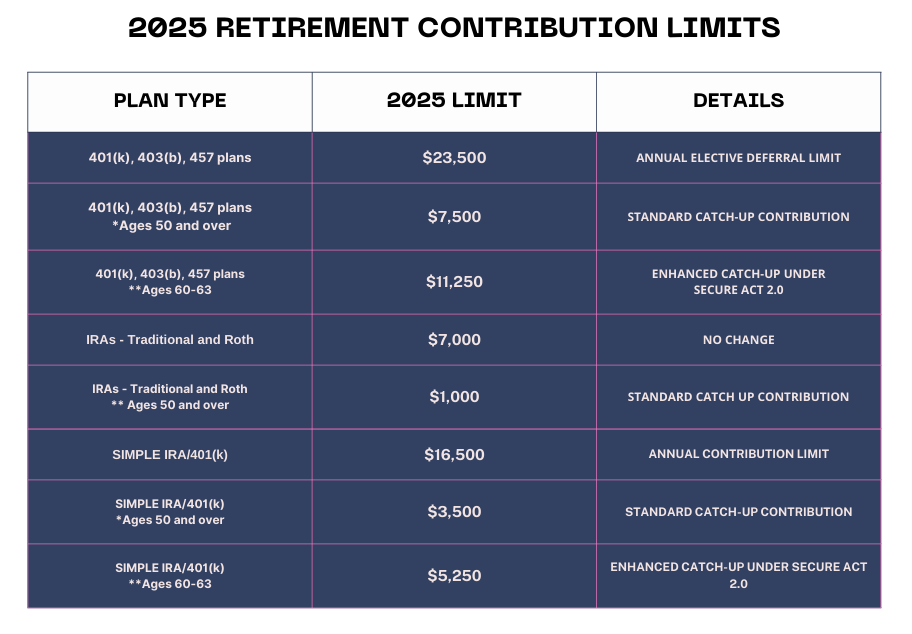

If you have recently inherited an Individual Retirement Account (IRA), it is important to understand the rules and options available to you to make informed financial decisions. Below are key points to guide you:

- Identify the Type of IRA

- Traditional IRA: Distributions will generally be subject to income tax.

- Roth IRA: Distributions are typically tax-free if the account has been open for at least five years.

- Determine Your Relationship to the original owner

- If you inherited the IRA from your spouse, you can treat the IRA as your own by transferring it into your name or roll it into your existing IRA. One advantage of transferring it to yourself is that required minimum distributions (RMDs) from a traditional IRA can be delayed until you turn 73 (75 if you were born in 1960 or later).

- If you inherited the IRA from someone other than your spouse, you cannot treat the IRA as your own. The requirement to take annual distributions from a traditional IRA is different depending on when the original owner died:

- If the original owner died before the required beginning date for RMDs, there is no required annual distribution, but the balance must be withdrawn by the 10th anniversary of the original owner’s death.

- If the original original owner died on or after the required beginning date, you must take annual distributions and have the entire amount withdrawn by the end of the 10th year after the original owner’s death. Very important to note: The IRA custodian is not required to notify you that RMDs are necessary.

- Exceptions may apply for eligible designated beneficiaries (e.g., minors, disabled individuals, or beneficiaries less than 10 years younger than the decedent).

- Understand Tax Implications

- Distributions from a Traditional IRA are taxable as ordinary income.

- Roth IRA distributions are tax-free if qualified

- Ensure you plan withdrawals to minimize your tax liability, possibly spreading them over multiple years.

By understanding these rules and options, you can better manage your inherited IRA to align with your financial goals. Please contact us for more information.

As we head into 2025, Wedel Rahill remains committed to looking ahead for tax planning opportunities for you, our valued clients. As your trusted advisors, we continually monitor legislative developments so that we can pass along pertinent tax policy changes that may impact you and your business.

While tax policy remains unpredictable when the country is experiencing a change in presidential administration, we believe the fundamental framework of the Tax Cuts and Jobs Act of 2017 will be extended and not allowed to expire. This provides stability in the income tax environment and allows us to offer tax planning strategies with confidence.

Based on current policy discussions, we anticipate the following for 2025 and near future:

-

- Lower individual tax rates across most tax brackets, maintaining the current seven-bracket structure.

-

- Preservation of the higher standard deduction amounts.

-

- Expanded Child tax credits (currently $2,000 per qualified child).

-

- Increased Alternative Minimum Tax exemption.

-

- Qualified Business Income (Section 199A) deduction continuation.

-

- Corporate tax rate to permanently remain at 21%.

-

- Section 179 expensing and bonus depreciation remain available.

With these extensions in mind, we want to help you strategically plan for the 2025 tax year. We can schedule individualized tax planning sessions to review your specific needs and circumstances. We pride ourselves on preparing accurate and timely tax projections for our clients and want to ensure you have no surprises when April 15, 2026 comes around. Please call our office to discuss how we can help.

This summary is intended for general information purposes only, and should not be construed as specific tax advice. Please consult with our firm for advice specific to your needs.

Have you noticed that in the past few years, people seem to be moving a lot? Many of those moves may be part of a tax planning strategy. According to a recent article in The Tax Adviser published by the American Institute of Certified Public Accountants, recent years have seen large numbers of taxpayers leaving high tax states in favor of states with lower income, property, sales, or estate tax rates. Retirees often choose to move to states with low- or no tax on pension and retirement distributions.

If you are considering making such a move, keep in mind non-tax implications of changing your state of legal residence. There is usually a trade-off when you make a decision solely for tax purposes. If, after considering all the factors, you wish to change your state residency, ensure you proceed with care. You may need to establish residency in your new state by fulfilling specific requirements. To change domicile successfully, a person needs to establish a new primary residence in another state and demonstrate their intent to make it their permanent home. The key steps to achieve this include:

-

- Establish Physical Presence

- Physically relocate to the new state and make it your primary residence. Spend the majority of the year there to establish a clear physical presence.

-

- Secure housing in the new state, whether by renting or purchasing a home.

- Establish Physical Presence

-

- Update Legal and Governmental Records

- Obtain a driver’s license or state identification card in the new state.

- Register your vehicle in the new state and update your insurance to comply with local laws.

- Register to vote in the new state to further demonstrate intent to reside there permanently.

-

- Change your mailing address through the postal service and notify banks, utilities, and other organizations.

- Update Legal and Governmental Records

-

- Establish Financial Ties

- Open accounts with banks in the new state.

- Start filing income taxes in the new state and, if applicable, as a part-year resident in your former state.

-

- Notify your employer of the move and ensure state income taxes are withheld appropriately.

- Establish Financial Ties

-

- Sever Ties with the Former State

- If you own property in your previous state, sell it or use it as a secondary residence, avoiding indications it remains your primary home.

-

- End memberships and affiliations tied to the former state, such as local clubs or organizations.

- Sever Ties with the Former State

-

- Demonstrate Intent

- Rewrite your will and other legal documents to reference the laws of the new state.

-

- Inform attorneys, accountants, and other advisors of your new residency.

- Demonstrate Intent

-

- Maintain Documentation

- Retain documents that demonstrate your move and activities, such as utility bills, moving receipts, and lease or purchase agreements.

-

- Record the number of days spent in the new state versus the old one to defend against any challenges to your residency.

- Maintain Documentation

-

- Engage in Community Life

- Participate in the community by joining local organizations, attending events, or volunteering.

-

- Establish care with local doctors and dentists to reinforce your connection to the new state.

- Engage in Community Life

If you move mid-year, you may need to file as a part-year resident in both states, allocating income earned in each jurisdiction accordingly. If your former state believes you haven’t fully cut ties, it may challenge your residency change and attempt to continue taxing you. Maintaining thorough records (e.g., lease agreements, utility bills, and voter registration) is crucial. By following these steps and maintaining clear records, individuals can substantiate their intent to change domicile, which is especially important for tax and legal purposes.